Retail traders often ask: “When should I buy?” Institutional traders ask: “What is the market structure right now?”

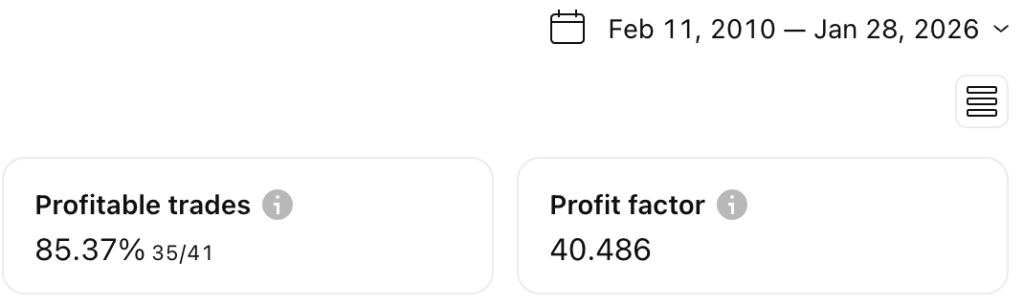

That distinction is why institutions survive crashes while retail accounts get wiped out. In my latest update to the TQQQ Master algorithm (v54), I moved away from simple technical indicators and integrated logic based on Market Structure and Volatility Regimes.

Here is the breakdown of the core ideas behind v54.

1. The VIX Term Structure (The “Tail Risk” Filter)

Most traders treat the VIX as a simple fear gauge. “If VIX is high, I’m scared.” But the raw number doesn’t tell the whole story. The relationship between short-term and medium-term volatility does.

- Contango (Healthy Fear): When Spot VIX is lower than 3-Month VIX (VIX3M). The market expects risk, but not right now. This is safe for trading.

- Backwardation (Panic): When Spot VIX spikes higher than VIX3M. This means investors are paying a premium for immediate protection. This is a “Tail Risk” event.

The v54 Logic: The algorithm monitors this spread in real-time. If Backwardation is detected, the system engages “Tail Risk Protocol.” Even if the chart technicals look perfect for a bounce, the system forces a defensive stance—reducing position sizing or halting new entries until the structure normalizes. This prevents catching the falling knife during a liquidation cascade.

2. The “Runner” Philosophy

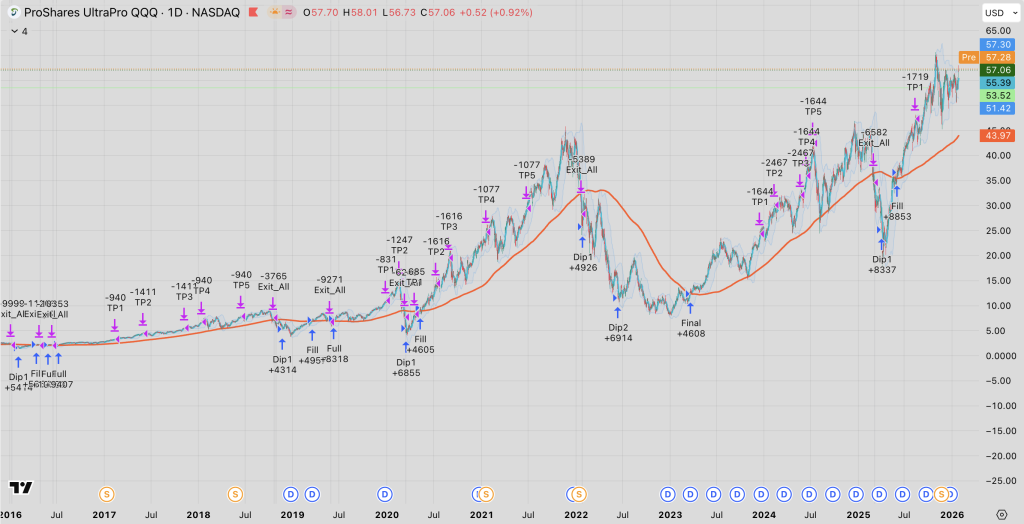

One of the biggest regrets in TQQQ trading is selling too early. You hit your +20% target, sell everything, and then watch the stock rally another 100%.

To solve this, v54 introduces a “Runner” system.

- Scale-Out: We take profits at 5 distinct levels (TP1 ~ TP5) to lock in gains and reduce risk.

- The Runner: However, we never sell 100%. The system is coded to keep 40% of the position as a “Runner.”

- The Rule: This Runner is held until the major trend (218 SMA) breaks. This ensures we participate in the “fat tail” of the bull market.

3. Filtering Volatility with QQQ

TQQQ is a noisy instrument. A -5% drop in TQQQ might just be a normal Tuesday. To filter this noise, the “Dip Buying” logic strictly references the underlying asset, QQQ.

- We buy TQQQ only when QQQ hits specific drawdown milestones (-15%, -25%).

- This prevents the algo from over-trading on leverage decay.

Conclusion

This update isn’t about finding a “Magic Indicator.” It’s about risk management. By respecting the VIX Term Structure, we acknowledge that not all dips are created equal. Some dips are opportunities; others are traps.

Note: This post shares the conceptual framework of my personal trading setup. The code is private, but I highly recommend adding VIX vs. VIX3M to your own manual watchlist.