Solar Module Pricing 2026 is being reset by a three-way squeeze: (1) trade enforcement that blocks “detour” supply chains, (2) China’s internal fiscal pivot that removes a key export incentive, and (3) a raw-material shock centered on silver—at the exact moment cell technology is becoming more silver-intensive.

If you model solar as a straight line of “modules get cheaper every year,” that assumption is now the risk—not the base case.

Solar Module Pricing 2026: Why the Old Cost Curve Just Broke

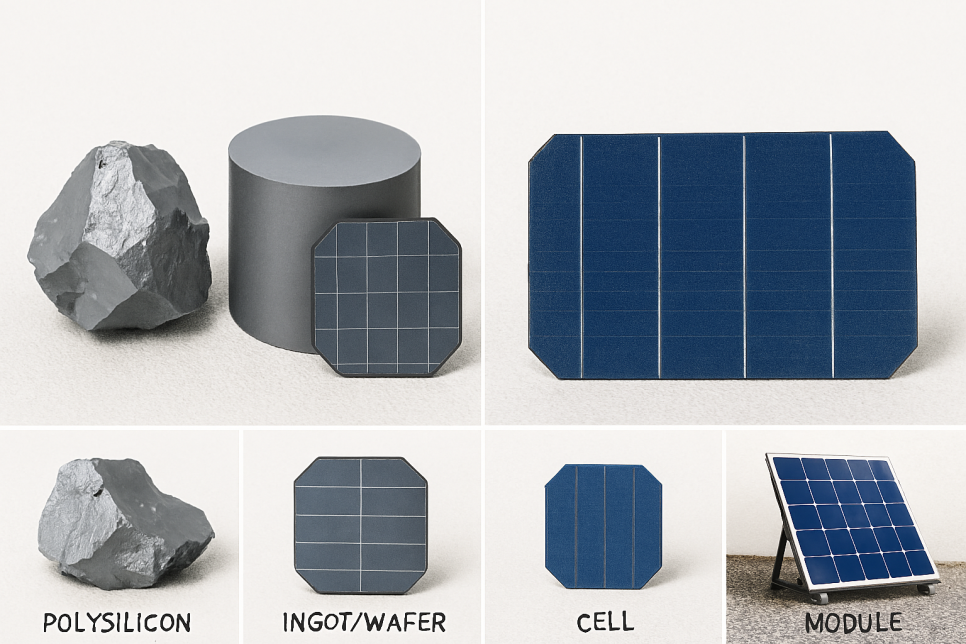

Start with the physical reality. Solar is not “one product”—it’s a value chain:

- Polysilicon → ingot/wafer → cell → module

For the last decade, the world’s deflationary solar story was powered by one thing: extreme supply-chain concentration. By 2024, International Renewable Energy Agency estimates China produced roughly ~79% of polysilicon, ~97% of wafers, ~85% of cells, and ~75% of modules globally.

That dominance matters because the most energy-intensive steps sit upstream. The International Energy Agency notes that electricity can be over 40% of polysilicon production costs (and nearly 20% for ingots/wafers).

In plain terms: cheap power + scale + vertically integrated factories made “China-priced solar” possible.

Now layer in the 2026 shift that most investors are still underweighting:

1) China is removing a pricing lever it used to defend exports

In January 2026, Reuters reported a joint announcement from China’s finance/tax authorities: VAT export rebates for photovoltaic products will be eliminated from April 1, 2026, and battery export rebates are cut (9% → 6%) through 2026 before ending January 1, 2027.

Mechanically, removing a 9% rebate is not “just 9%.” In a multi-stage chain (wafer → cell → module), each step adds handling cost, yield loss, logistics, and margin. That compounding is why market pricing can move far more than the headline rebate change. (This is especially true when producers have any ability to reprice after a long price war.)

2) Silver is no longer a rounding error

Silver is the “hidden input” that becomes painful precisely when you upgrade cell tech.

- Industry snapshots (IEA PVPS materials) show typical silver intensity rising from PERC (~7–8 mg/W) to TOPCon (~12–16 mg/W) and HJT (~17–20 mg/W).

- By early 2026, PV-focused reporting indicates silver has overtaken polysilicon as a leading cost driver, with silver around ~16–17% of total module costs in some estimates.

- Broader market coverage also flags episodes where silver becomes an even larger share during spikes.

This is the uncomfortable math: the industry wants higher-efficiency cells, but higher-efficiency cells want more silver—right when silver is expensive.

3) Incentives are no longer “set-and-forget” in the U.S.

Policy risk is not theoretical. The Internal Revenue Service reflects that the residential clean energy credit window is constrained through 2025 under recent law changes/implementation guidance.

At the utility/commercial level, multiple 2025 policy updates have effectively turned tax credits into a deadline-driven financing variable, not a perpetual backstop.

Put it together and the message is simple: costs are rising at the same time financing certainty is getting harder. That is how an industry goes from “volume solves everything” to “margins and cancellations suddenly matter.”

Trade Enforcement Is Closing the “Detour” Route

For investors, the key structural change isn’t just tariffs—it’s enforcement credibility.

The forced-labor constraint moved from headline risk to operational risk

The Uyghur Forced Labor Prevention Act became enforceable in June 2022, creating a rebuttable presumption for goods tied to Xinjiang-linked supply chains.

Predictably, production and finishing steps shifted toward Southeast Asia. In practice, the U.S. ended up heavily dependent on modules routed through four countries: Cambodia, Malaysia, Thailand, and Vietnam—with reporting suggesting a dominant share of imports coming via that channel.

Then the U.S. slammed the economics of the workaround

In April 2025, the U.S. Department of Commerce announced final affirmative AD/CVD determinations on crystalline PV cells (including those assembled into modules) from those four Southeast Asian countries.

The headline that stuck: tariff rates reaching as high as 3,521% for certain exporters—numbers that functionally say “this product is not welcome at any normal price.”

CBP tightened the visibility layer in 2026

In January 2026, U.S. Customs and Border Protection rolled out a revamped forced-labor site and an updated enforcement dashboard with more granular transaction-level details and filtering (including commodity classifications and country-of-origin fields).

This matters because “I bought it from Country B” is less useful when enforcement can pressure-test the chain at a finer level.

Europe is converging (with a long fuse)

The European Commission states the EU forced-labor regulation will apply from 14 December 2027.

That is a delayed hammer—but it still changes how global suppliers plan capacity today, because you don’t re-architect a solar supply chain in a quarter.

Demand is still huge—so repricing hits hard

The U.S. solar buildout remains structurally large. U.S. Energy Information Administration projected solar would be 58% of new U.S. utility-scale capacity additions in 2024.

In other words, the system is trying to install more solar even as the “cheap module pipeline” gets politically and fiscally constrained.

That is exactly how you get pre-buying/stockpiling behavior, project re-bids, delayed CODs, and a slow-motion reset of IRRs across the developer universe.

The solar story is not “over,” but the easy version of it is. When supply chains are concentrated, enforcement tightens, and China removes a key export rebate at the same time silver gets expensive, the market doesn’t glide—it reprices. Solar Module Pricing 2026 is the line item that will force investors to revisit assumptions across solar developers, installers, equipment suppliers, and—importantly—competing generation sources that look better when solar’s marginal cost rises.

[TMM’s Perspective]

I don’t treat this as a one-week headline; I treat it as a regime shift in how solar gets financed and procured. We’re watching a classic transition from “policy tailwind + manufacturing deflation” to “policy fragmentation + input inflation,” and markets usually misprice that transition at first. If you’re investing around power generation, I would stress-test every thesis against two variables: module availability under trade rules and project economics under tighter tax-credit windows. And yes—when solar’s cost of capital and hardware cost rise together, I start paying closer attention to the relative setup for nuclear and other firm power.