The market narrative is shifting decisively. For years, investors huddled in the safety of mega-cap tech and recession hedges like gold. However, data from mid-January 2026 suggests the “uncertainty premium” is evaporating.

The latest “Lunch Briefing” data indicates a structural rotation is underway. We are witnessing a convergence of fading tariff risks, a resurgence in the real economy (manufacturing), and a liquidity spillover from conservative funds into risk assets.

Here is the breakdown of why the smart money is moving into Small Caps and why the “Recession Fear” trade might be over.

1. The Russell 2000 Awakening

The most significant signal in the current market isn’t found in the Nasdaq 100, but in the Russell 2000 (IWM). Small-cap stocks have outperformed the broader market for 10 consecutive trading days—a streak not seen since 1990.

Technically, the Russell 2000 is breaking above its “Corona Bubble” peak from 2021.

- The Implications: When small caps break all-time highs, it historically triggers a sequence of liquidity flow: Small Caps → High Growth (e.g., ARKK) → Crypto Assets.

- The Losers: Conversely, this risk-on environment typically suppresses defensive assets like Gold and Silver, which tend to stagnate or correct as capital seeks higher beta returns.

2. The Real Economy is Roaring Back

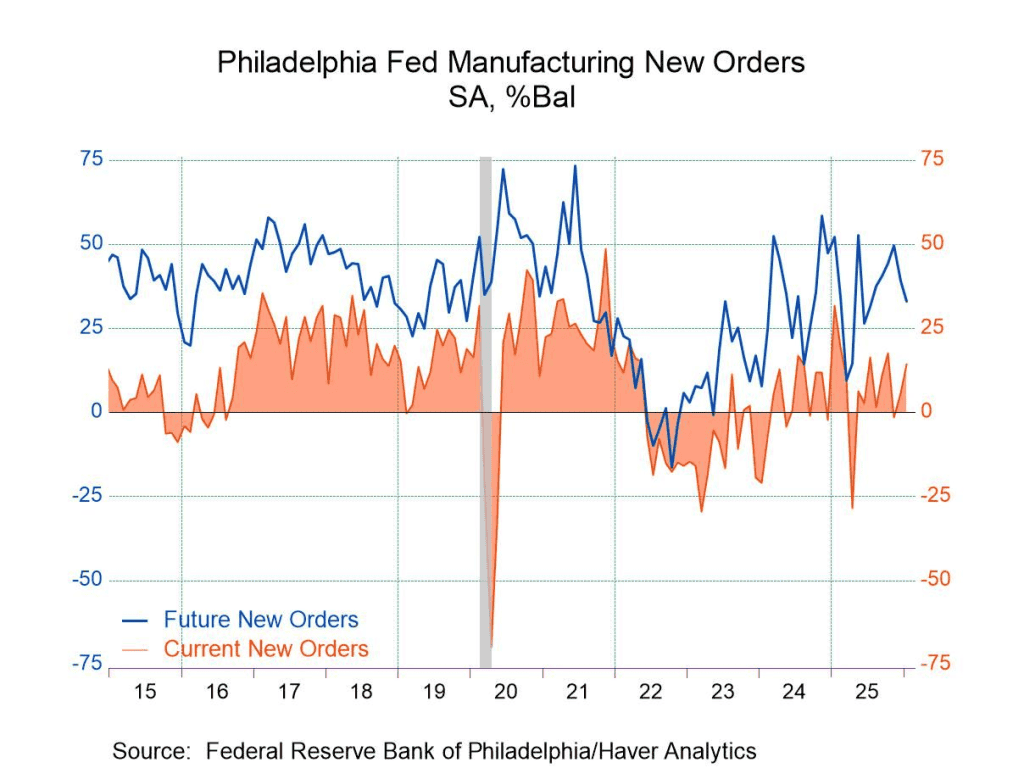

The bear case for 2026 relied heavily on a manufacturing recession. Yesterday’s data shattered that thesis.

- Philadelphia Fed Manufacturing Index:

- Forecast: -1.6 (Contraction)

- Actual: 12.6 (Strong Expansion)

- NY Empire State Manufacturing Index:

- Forecast: 0.8

- Actual: 7.7

This massive beat indicates that the industrial economy is not just stabilizing but accelerating. Furthermore, Initial Jobless Claims dropped to 198k (vs. 215k expected), reaffirming that the labor market remains tight despite previous fears.

3. The “Tariff Bluff” and Corporate Confidence

Why is manufacturing rebounding so aggressively? The lifting of the “Tariff Fog.”

Throughout 2025, businesses paused CapEx due to fears of a trade war. However, the Trump administration’s recent moves confirm that tariffs are being used as leverage, not a suicide pact.

- Semiconductors: Imported chips for data centers and AI are largely exempt.

- Taiwan: Tariffs reduced to 15%.

- Critical Minerals: No tariffs imposed (the “TACO” negotiation strategy).

This policy clarity has unleashed pent-up corporate spending. TSMC just announced a $56 billion CapEx plan for 2026 (up from $40.9B in 2025), with the CEO explicitly stating, “AI is real,” after meeting with major cloud providers.

4. The Liquidity Floodgates Open

Perhaps the most bullish metric for equities is the movement in Money Market Funds (MMF).

For nearly two years, MMF assets climbed, acting as a massive reservoir of sideline cash. This week, we saw a critical inflection point:

- MMF Total Assets: Decreased from $7.8 Trillion to $7.72 Trillion.

The curve is flattening and beginning to roll over. This signifies that capital is leaving safe havens (yielding ~4-5%) and chasing the equity risk premium. As this $7 trillion wall of money enters the market, it naturally flows into under-owned assets like small caps and industrials.

MMF assets are stalling and beginning to decline, a classic leading indicator for risk-asset appreciation.

5. Global Green Shoots

The recovery isn’t isolated to the US.

- Germany: GDP grew +0.2%, exiting negative territory for the first time in 3 years.

- UK: GDP posted a surprise +0.3% growth (beating 0.1% estimates).

Synchronized global growth provides a floor for commodity prices (specifically industrial metals like Copper) while putting pressure on the US Dollar, further aiding US multi-nationals.

TMM’s Perspective

“The market hates uncertainty more than it hates bad news. Throughout 2025, we dealt with the threat of tariffs. Now, we have the reality of exemptions.

The data presented today confirms our thesis: We are in an early-cycle recovery, not a late-cycle bust. The rotation into the Russell 2000 is healthy; a bull market cannot survive on Nvidia alone.

Actionable Insight: The risk/reward for Gold is deteriorating in the short term as real yields likely rise with better growth data. The ‘Catch-up Trade’ in Small Caps (IWM) and Biotech (XBI/ARKK) offers significantly higher upside potential as MMF liquidity seeks yield.”

Disclaimer: This content is for informational purposes only and does not constitute financial advice. Investment involves risk.

1 thought on “The Great Rotation 2026: Why Small Caps and Manufacturing Are Leading the Rally”