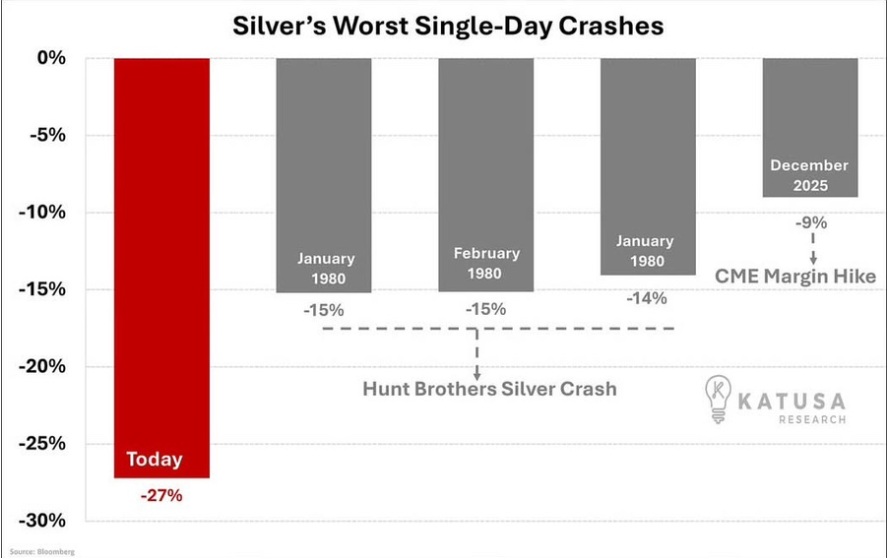

Silver Price Crash 2026 wasn’t “just a bad day”—it looked like a classic liquidity cascade where leverage, positioning, and policy headlines hit the market at the same time. When I see a one‑day move on the order of ~27% in a major futures market, I stop asking “what’s the narrative?” and start asking “what broke in the plumbing?”

I’m going to do two things in this post:

- separate the documented (margin changes, regulatory actions, and confirmed enforcement history) from the speculative (the “someone handed the short to someone else” storyline), and

- explain why this matters even if you’re a U.S. stock investor who never touches a futures contract.

Silver Price Crash 2026: The Mechanical Triggers No One Can Ignore

When a market is heavily levered, the “trigger” is often boring: margins, market structure, and forced selling—not a single villain and not a single headline.

1) Margin hikes: the most underappreciated “off switch”

If you want to understand how fast a crowded trade can unwind, study what happened to the Hunt brothers: an epic silver squeeze fueled by leverage, followed by exchange rule changes and margin pressure that helped flip momentum into liquidation.

That same mechanism shows up repeatedly in modern episodes. For example, CME Group clearing notices show that late‑December 2025 “performance bond” requirements (margin) were raised—COMEX 5,000‑oz silver futures moved from $22,000 to $25,000 per contract (roughly +14%), while COMEX 100‑oz gold futures moved from $20,000 to $22,000 (+10%).

And the tightening didn’t stop there. A later clearing advisory dated January 30, 2026 shows silver margin parameters moving from 11% to 15% (with higher‑risk tiers also increasing).

My takeaway: margin doesn’t care about your conviction. If you’re levered, margin forces your hand—fast.

2) “HFT + microstructure” is not a side plot anymore

I’m not here to demonize high‑frequency trading. Speed and automation can add liquidity—until they don’t.

What matters for investors is the fragility this creates when regulators change the rules of the game mid‑stream. In early 2026, China moved to remove the speed advantage of certain market participants by ordering the removal of servers housed in exchange data centers (a direct shot at co‑location style advantages).

Then, right as volatility peaked, Chinese authorities also moved to halt trading/subscriptions in certain commodity fund products—among them the UBS SDIC Silver Futures Fund—which can mechanically reduce marginal demand if the product must add futures/hedges when new money flows in.

My takeaway: if liquidity was being “manufactured” by fast traders or by fund‑flow‑driven buying, a sudden regulatory clampdown can make the order book feel empty at exactly the wrong moment.

3) Policy shock: the dollar narrative flipped

The macro layer matters too—especially for precious metals. Reports tied the metals selloff to shifting expectations after Donald Trump nominated Kevin Warsh to lead the Federal Reserve, alongside a broader “stronger dollar / tighter stance” interpretation that can weigh on gold and silver.

The U.S. Treasury’s messaging also matters here, and Scott Bessent has been part of the policy backdrop investors are reacting to.

4) One 2026 wrinkle investors shouldn’t ignore

Here’s a very 2026‑specific detail: CME announced a smaller 100‑ounce silver futures contract (positioned as a retail‑friendly instrument). That kind of product decision usually shows up when participation broadens—and broad participation often means more momentum, more leverage, and more violent reversals.

Bottom line: the Silver Price Crash 2026 reads like a “layered risk” event—momentum + leverage + margin tightening + policy repricing + a sudden microstructure shock. I don’t think any single factor explains the full move.

From Bear Stearns to JPMorgan: Spoofing, Physical Silver, and the BofA Theory

Now for the part people actually forward to friends.

The “dealer problem” that starts in 2008

Bear Stearns was an old‑line Wall Street firm (founded in 1923) that collapsed during the 2008 crisis and entered a merger agreement with JPMorgan Chase in March 2008.

The key idea in your original Korean thesis is simple—and it’s structurally true even outside silver:

- Hedge funds and institutions often use futures/options to hedge exposures or express macro views.

- Dealers (banks/prime brokers) frequently end up “making the market” as counterparties.

- If clients pile into the same trade (e.g., “hedge by shorting silver”), the dealer can accumulate a very large offsetting exposure over time.

In the silver community’s version of events, Bear Stearns was rumored to have built an enormous silver‑related short while intermediating client flow. When JPMorgan took over Bear Stearns, the theory goes, it inherited that exposure.

What’s documented vs. what’s “market lore”

Here’s what is documented: JPMorgan’s precious‑metals desk became the focus of major U.S. enforcement.

- The Commodity Futures Trading Commission said the conduct involved spoofing and manipulation spanning at least eight years and hundreds of thousands of spoof orders in precious metals and U.S. Treasuries, and it announced a record $920 million resolution.

- The U.S. Department of Justice described schemes to defraud in precious metals and Treasuries and a deferred prosecution agreement tied to that ~$920 million figure.

- The Securities and Exchange Commission also announced related enforcement action.

That is not conspiracy. That is public record.

Now, here’s what remains speculative (and I’m labeling it that way on purpose):

- The “physical hedge” story. The claim is that JPMorgan didn’t simply close inherited shorts—it allegedly hedged by accumulating a massive physical silver position over many years, because physical inventory can offset losses on a paper short when silver rises. This is plausible in structure, but hard to confirm in precise size because physical holdings are not transparently reported in a single clean dataset.

- The “hot potato” story: JPMorgan → Bank of America. The conspiracy theory in your text starts when JPMorgan’s short exposure supposedly fades (post‑settlement), while another large bank’s short exposure grows—most commonly Bank of America. The argument is that “money has no tag,” so we can’t prove a direct transfer—but the timing looks suspicious to commentators.

Here’s the sober reality: public positioning data (like the CFTC’s Bank Participation Reports) is aggregated—it can show how many banks are long/short and by how much, but it generally does not hand you a neat “Bank X holds Y” map. That’s exactly why these narratives thrive: there’s a real information gap.

Why the theory got louder in 2025–2026

Even without asserting a secret deal, the incentives are straightforward:

- If a firm is short paper silver without a robust hedge, a violent upside move can become existential.

- If another firm is long physical or otherwise structurally hedged, it can survive the same move—or even profit.

So the “BofA got stuck holding the bag” storyline is emotionally satisfying. But it is still not proven.

What I take from this as an investor:

- I treat “conspiracy narratives” as signals of where positioning may be fragile, not as courtroom evidence.

- I watch the boring stuff—margins, funding stress, and rule changes—because that’s what forces liquidation.

If you want one clean explanation for a one‑day 27% collapse, you’ll be disappointed. The more realistic answer is layered: margin pressure can force selling, microstructure rules can thin liquidity, and macro policy can flip sentiment—all while the market argues about who’s secretly on the other side of the trade. That’s the real lesson of the Silver Price Crash 2026: the “why” is often less important than the “how.”

[TMM’s Perspective]

I don’t try to “out‑speed” machines or out‑lawyer regulators—I try to avoid getting forced. I size smaller when an asset has gone parabolic, and I assume margin changes can arrive at the worst possible moment. I also treat extreme one‑day moves as liquidity events first and valuation events second. And if I’m investing through equities (miners, royalty names, suppliers), I remember the futures market can drag those stocks around even when the company fundamentals didn’t change overnight.