The Fed Independence Crisis of early 2026 has escalated into a constitutional standoff following the Department of Justice’s decision to issue a grand jury subpoena to Federal Reserve Chairman Jerome Powell. What ostensibly began as an investigation into budget overruns regarding the Eccles Building renovation has rapidly morphed into a proxy war over monetary sovereignty. With the 10-year Treasury yield showing hypersensitivity to political instability this quarter, investors must look past the headlines to understand the structural deadlock forming in the Senate Banking Committee.

The Catalyst of the Fed Independence Crisis: The Eccles Building Renovation

The ostensible trigger for this legal confrontation lies in the renovation of the Federal Reserve’s headquarters. The Eccles Building, completed in 1937, has been undergoing extensive remodeling since 2022. While originally budgeted at $1.8 billion, costs have reportedly ballooned to $2.5 billion—a $700 million excess—with the completion date pushed from late 2023 to 2027.

While delays in restoring a registered historic landmark are not uncommon in Washington, the scrutiny focuses on alleged “luxury upgrades.” The proposal submitted to the Senate reportedly included amenities such as a VIP-exclusive elevator, fountains, marble fixtures, and a rooftop terrace.

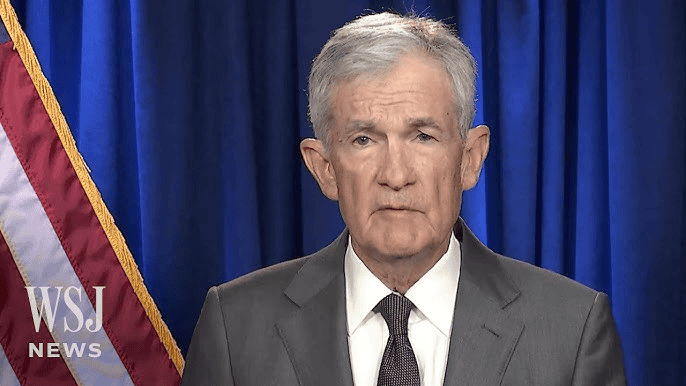

However, during a June 2025 Senate hearing, Chairman Powell explicitly denied these inclusions. In a direct rebuttal to the allegations of excess, Powell testified:

“The headquarters building was in an unsafe condition. Waterproofing was not functioning properly. There is no VIP dining room, no new marble, and no special elevator. There are only the old elevators that were there before, and there are no artificial waterfalls, apiaries, or rooftop terrace gardens.”

The Grand Jury subpoena aims to determine if this testimony constitutes perjury. However, for institutional investors, the specifics of the renovation are secondary to the broader Fed Independence Crisis aimed at pressuring the central bank’s policy committee.

Powell Strikes Back: Defending Monetary Policy

The timing of this investigation—orchestrated by a U.S. Attorney with close ties to the administration—suggests motivations beyond fiscal auditing. Chairman Powell addressed the media in an emergency press conference, framing the subpoena not as a legal inquiry, but as a direct assault on the Federal Reserve’s dual mandate.

Powell provided the following statement regarding the escalation:

“On Friday, the Department of Justice served the Federal Reserve with a grand jury subpoena. The content foreshadowed criminal indictment. It relates to the testimony I gave before the Senate Banking Committee last June. That testimony was, in part, regarding the Fed’s historic building renovation project that has been ongoing for years.

I deeply respect the rule of law and democratic accountability. No one, not even the Fed Chair, is above the law. However, this unprecedented action must be viewed in the broader context of threats and persistent pressure from the administration. This new threat is not about my testimony last June or the Fed building renovation. Nor is it about Congress’s oversight role. The Fed has made every effort to fully inform Congress about the renovation project through testimony and other public materials. These are merely pretexts.

The threat of criminal prosecution is the result of the Fed deciding interest rates based on its best judgment to serve the public interest, rather than the President’s preferences. This is a question of whether the Fed will be able to continue deciding rates based on evidence and economic conditions, or whether monetary policy will be swayed by political pressure or intimidation.”

Powell concluded his defense by affirming his refusal to resign, despite his term as Chair ending in May 2026:

“I have served the Fed under four administrations, both Republican and Democratic. Each time, I have performed my duties without political fear or bias, focusing solely on our mandate of price stability and maximum employment. Public service sometimes requires standing firm in the face of threats. I will continue to carry out the duties confirmed by the Senate with integrity and a sense of mission for the American people.”

Legislative Gridlock: The Mathematical Reality of the Fed Independence Crisis

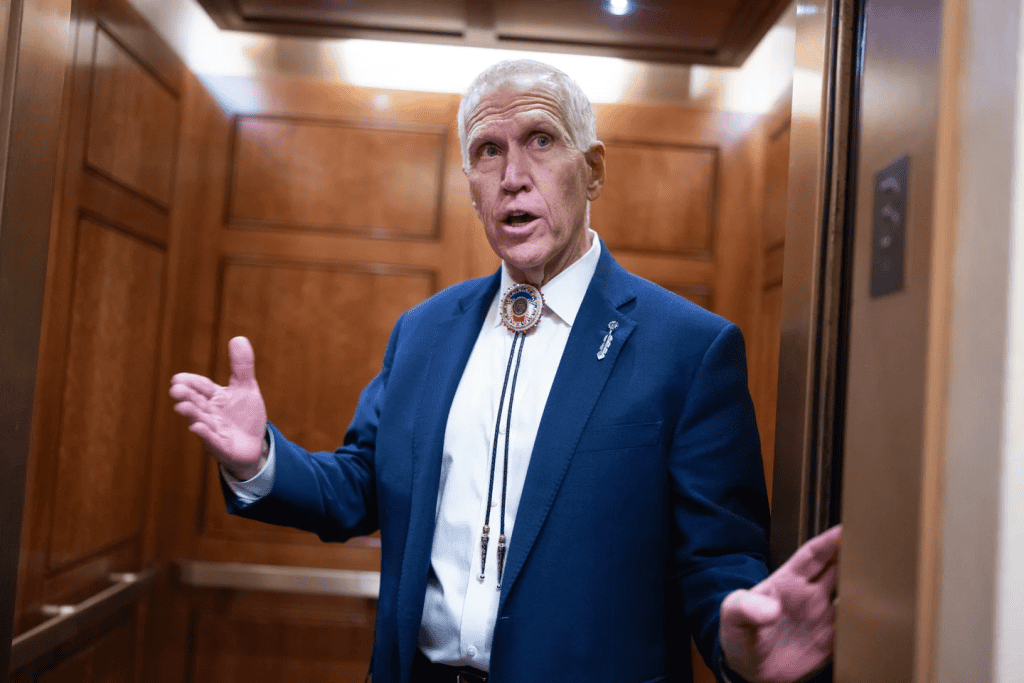

The most immediate risk to the market is not the investigation itself, but the paralysis of the Senate Banking Committee. On January 13, Republican Senator Thom Tillis issued a statement that effectively freezes the confirmation process for any new Federal Reserve nominees.

Tom Williams via Getty Images

Senator Tillis stated:

“I had doubts that Trump administration staff were actively working to undermine the Fed’s independence, but those doubts are now completely gone. The independence and credibility of the Department of Justice are in question. Until this issue is fully resolved, I will oppose the confirmation of all Federal Reserve Board nominees, including the Chair.”

This creates a severe bottleneck. The Senate Banking Committee consists of 24 members: 13 Republicans and 11 Democrats. Confirmation requires a majority to reach the Senate floor. If Senator Tillis votes with the Democrats, the vote becomes a 12-12 tie. In the event of a tie, the nomination is stalled and cannot proceed to a full Senate vote.

Furthermore, even if a nominee were to bypass the committee, the Fed Independence Crisis empowers the use of the filibuster. With the current Senate composition (53 Republicans, 45 Democrats, 2 Independents), breaking a filibuster requires 60 votes. This legislative arithmetic suggests that the White House will be unable to install a preferred successor to Powell or fill vacant Governor seats, potentially leaving the Fed understaffed or in a zombie state during a critical economic cycle.

[Image Placeholder 1]

- Description: A split image showing the exterior of the Eccles Building under construction on one side, and Jerome Powell testifying on the other.

- Alt Text: Jerome Powell testifying before Congress regarding the Fed Independence Crisis and Eccles Building renovation.

- Caption: The renovation of the historic Eccles Building has become the flashpoint for a battle over monetary policy independence.

Conclusion

The Fed Independence Crisis is no longer a theoretical risk; it is a mechanical reality within the US legislative process. While the Grand Jury investigation grabs headlines, the true market signal lies in Senator Tillis’s pivot. By blocking the Senate Banking Committee’s ability to confirm nominees, the path for a politically compliant Fed Chair is effectively closed. As we move deeper into 2026, the market must price in a scenario where the Fed operates under siege, potentially leading to higher volatility in sovereign debt markets.

[TMM’s Perspective]

The implications of Senator Tillis’s rebellion cannot be overstated. We are moving from a narrative of “political pressure” to actual “institutional paralysis.” If the Trump administration responds aggressively to this legislative blockade, we expect a rapid repricing in safe-haven assets. Specifically, Gold (XAU/USD) and Silver are likely to decouple further from real rates as they begin to price in the systematic risk of a compromised central bank. Investors should monitor the spread between 2-year and 10-year yields closely; any further flattening in response to this political noise acts as a buy signal for hard assets.